What Lenders, Insurers, and Homebuyers Are Looking At in 2026

Buying, selling, insuring, or refinancing a home in Florida has become more complicated than it was just a few years ago — and the roof is often at the center of the conversation. Across Palm Beach County and throughout the state, insurance underwriting reviews, mortgage-lender conditions, and property inspections increasingly turn on a single question about the roof: what condition is it actually in, and how much serviceable life does it have left?

Many homeowners assume the only thing that matters is how old the roof is. In reality, lenders, insurers, underwriters, and buyers are paying far closer attention to roof condition, remaining useful life, wind mitigation features, insurability, and — above all — documentation. A properly documented roof with serviceable life remaining can be far more valuable in a transaction than a newer roof with undocumented issues.

This guide explains what each party in a Florida real estate or insurance transaction is really looking at in 2026, how Florida’s Roof Age Law and wind mitigation reporting fit in, and why a documentation-first approach protects homeowners, buyers, sellers, agents, associations, and lenders alike.

Can an Older Roof Prevent a Home Sale?

An older roof does not automatically prevent a home sale — but an undocumented roof can stall one. When a roof becomes an obstacle in a Florida transaction, it is usually because one or more of the following reviews raised a question that no one could answer with paperwork:

- Insurance underwriting. Before a policy is issued or renewed, carriers evaluate the roof’s condition and expected service life. Without a current inspection, an underwriter may default to the most conservative assumption.

- Mortgage lender requirements. Lenders generally want assurance that the property is insurable and that the roof will not require immediate major expense. If a buyer cannot bind insurance, the loan can be delayed or denied.

- Remaining useful life evaluations. Increasingly, the deciding factor is not the roof’s age but a documented estimate of how many years of service it has left.

- Property inspections. A home or four-point inspection may flag the roof; a qualified roofing evaluation can clarify whether the finding is cosmetic, isolated, or genuinely material.

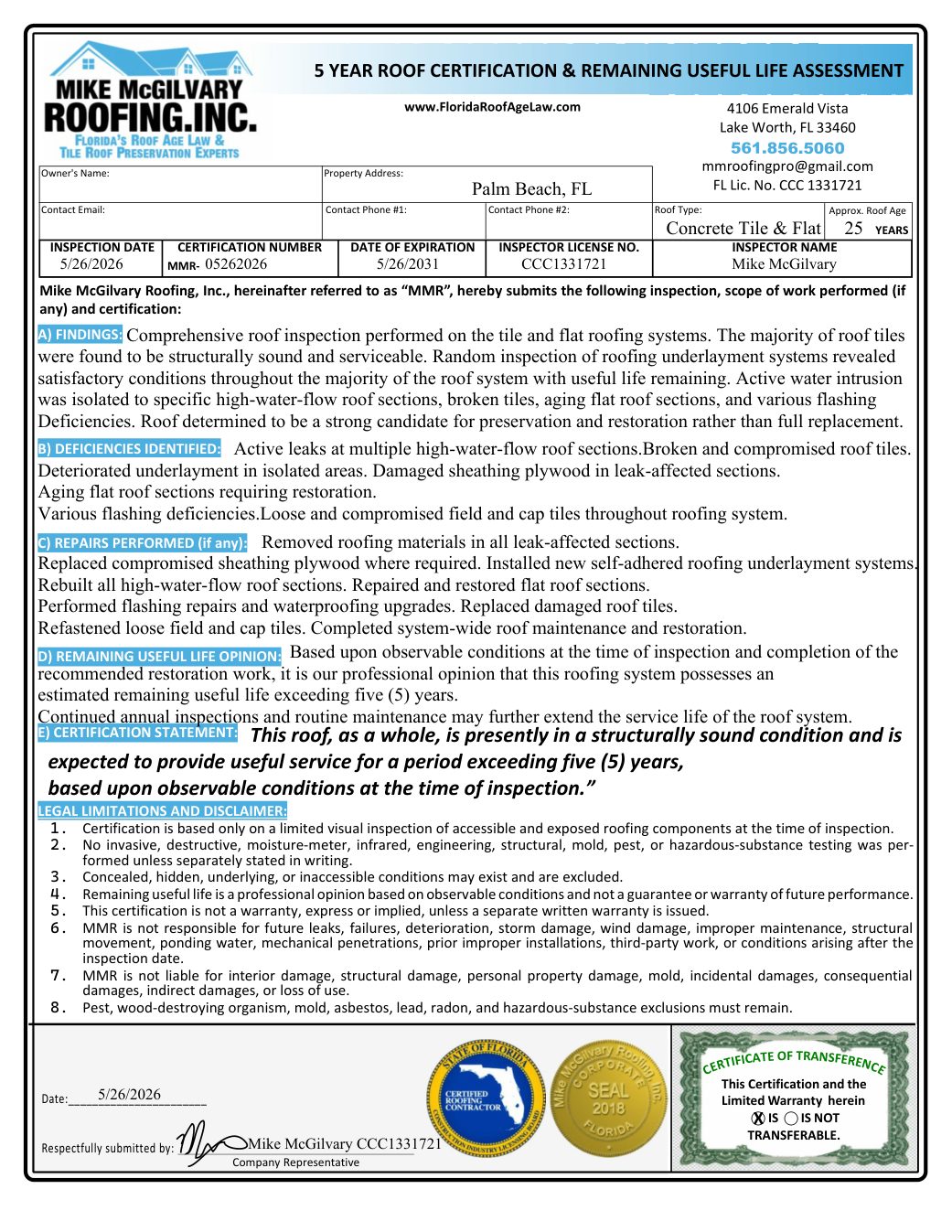

- Roof certifications. A signed roof certification from a licensed contractor gives every party a clear, professional statement of the roof’s condition and serviceable life.

In other words, the problem is rarely the roof’s birthday. The problem is the absence of credible, current documentation — and that is something a properly performed inspection can solve.

What Is Remaining Useful Life (RUL)?

Remaining useful life is a professional estimate of how many years a roof can be expected to continue performing — protecting the structure and keeping water out — based on its present condition rather than its installation date.

This is the single most important distinction for Florida property owners to understand. Two roofs installed in the same year can have completely different life expectancies. One may have been maintained, repaired in the right places, and kept watertight. The other may have neglected flashings, deteriorated underlayment, or failed valleys that quietly shorten its service life. Age looks identical on paper; condition tells the real story.

When our inspectors evaluate a roof, they assess the actual drivers of roof failure — underlayment condition, flashings, valleys, roof-to-wall transitions, penetrations, fastening, and water-management details — and translate those findings into a documented remaining-useful-life assessment that buyers, sellers, agents, insurers, and lenders can rely on.

Condition matters more than age.

Florida Roof Age Law: What Homeowners Need to Know

Florida law has helped move the insurance conversation away from age and toward condition. Under Florida Statute §627.7011, the focus for many roofing systems is on documented condition and remaining useful life rather than age alone.

For Florida homeowners, the practical takeaways are straightforward:

- Age alone should not automatically trigger a denial. A roof with meaningful serviceable life remaining may still qualify for coverage even when it is no longer new.

- Inspections matter. A current, professional roof inspection is what demonstrates condition and remaining useful life — the facts carriers and lenders actually evaluate.

- Documentation matters. An inspection only helps if it is captured in clear, professional paperwork that can be shared with insurers, agents, and lenders.

We cover this topic in depth on our Florida Roof Age Law resource. Insurance and statutory requirements change over time and vary by carrier and policy, so homeowners should confirm current specifics with the statute itself and with their insurance professional — the disclaimer at the end of this article explains why.

How Wind Mitigation Reports Affect Insurance and Mortgage Transactions

In Florida, wind mitigation features are documented on the state’s updated Uniform Mitigation Verification Inspection Form (OIR-B1-1802). A wind mitigation inspection records the construction and condition characteristics that influence how a home performs in high winds, including:

- Roof deck attachment — how the roof sheathing is fastened to the structure.

- Roof-to-wall connections — clips, straps, or other connectors tying the roof to the walls.

- Secondary water resistance — a sealed or supplemental barrier beneath the roof covering that helps keep water out if the primary covering is compromised.

- Opening protection — impact-rated or shuttered windows, doors, and other openings.

- Documentation requirements — the photographs and verifications the form requires for each feature to be credited.

Strong, well-documented wind mitigation features may help improve a home’s insurability and may support premium credits when applicable — and a clean, complete report removes a common source of friction in a real estate transaction. (Whether any particular credit applies is determined by the insurer and the policy, not by the contractor.)

The Difference Between Roof Replacement and Roof Preservation

One of the most expensive misconceptions in Florida roofing is that an aging roof must be torn off and replaced. Many roofs do not require immediate replacement at all.

- High-water-flow areas can often be rebuilt. Valleys, roof-to-wall transitions, skylights, and flashings age faster than the rest of the roof and can frequently be rebuilt or restored on their own.

- Tile systems can often be preserved. On many Florida tile roofs, the tile itself outlasts the waterproof layer beneath it. The sound tile can be lifted and re-laid over new underlayment — a tile roof preservation approach — often through a targeted roof rebuild rather than a full tear-off.

- Targeted repairs can extend service life significantly. Addressing known points of failure before they spread is the difference between a measured repair and an avoidable replacement — an honest repair-versus-replacement decision made on documented facts.

On numerous Palm Beach County projects — in communities from Palm Beach and West Palm Beach to Boca Raton, Delray Beach, Boynton Beach, Wellington, and Jupiter — we have issued roof certifications after performing targeted repairs and rebuilding high-water-flow areas, giving owners and buyers documented proof of a roof’s condition and serviceable life without the cost and disruption of a full replacement.

What Realtors, Buyers, and Property Managers Should Request

If you are buying, selling, insuring, or managing a Florida property, the goal is simple: replace uncertainty about the roof with documentation. Before closing or renewal, request the following:

- ✓Roof Certification

- ✓Remaining Useful Life Evaluation

- ✓Wind Mitigation Inspection

- ✓Repair Documentation

- ✓Before-and-After Photos

- ✓Permit History

- ✓Annual Inspection Plan

Each of these items answers a question someone in the transaction would otherwise have to guess at. Together, they turn the roof from a source of risk into a documented asset. A comprehensive roof inspection is where that documentation begins.

Mike McGilvary Roofing’s Documentation-First Approach

Mike McGilvary Roofing is a Florida-licensed roofing contractor focused on condition-based roofing and documentation. We position our work around the specific areas that decide modern Florida transactions:

- Florida Roof Age Law — helping owners understand how condition and remaining useful life fit the framework of §627.7011.

- Roof certification — signed certifications for insurance and real estate transactions.

- Tile roof preservation — saving sound tile roofs instead of replacing them by default.

- Documentation — clear, professional records that every party to a transaction can rely on.

Most roofing companies provide a proposal. Mike McGilvary Roofing provides documentation that helps homeowners, buyers, insurers, agents, associations, and lenders make informed decisions.

That difference — documentation over a sales proposal — is why agents, property managers, and homeowners across Palm Beach County and beyond, including markets like Tampa, turn to us when a roof needs to clear insurance or lending review. Our work and credentials have also been recognized in regional news and media coverage.

If you have a roof that needs to be evaluated, documented, or certified for an insurance renewal, a sale, or peace of mind, request a comprehensive inspection or call (561) 856-5060.

Mike McGilvary Roofing, Inc.

Florida Certified Roofing Contractor CCC1331721

Florida’s Roof Age Law & Tile Roof Preservation Experts

Reviewed by Mike McGilvary — Florida Certified Roofing Contractor, License CCC1331721.

Disclaimer: This article is provided for general educational purposes and does not constitute legal, insurance, or financial advice. Florida statutes, insurance underwriting standards, and lender requirements change over time and vary by carrier, policy, and property. Nothing here guarantees any insurance, lending, or coverage outcome. Always confirm current requirements with the applicable statute, your insurance professional, and your lender, and rely on a licensed contractor’s inspection of your specific roof.

Related from Mike McGilvary Roofing